Key points

- We expect inflation and interest rates to persist at higher levels than in the previous market regime.

- Alongside this, elevated levels of post-Covid government debt create a drag on economies which, in turn, can lead to broadly more volatile market returns.

- With governments needing to maintain spending on health and defence, the appetite for fiscal policy to support growth is undermined by the interest bill.

- When the market trinity of inflation, debt and interest rates is on the rise, market anxiety rises, as does higher volatility.

- We believe we have entered this phase but there are early signs that calm can return.

It might appear to be stating the obvious, but for markets to be in a good mood, the market ‘trinity’ of inflation, debt and interest rates, all need to be well behaved. All three indicators are connected, of course, but if inflation remains stable and at low levels, interest rates do not need to be too elevated. Meanwhile, if government debt is stable and not too much of a burden, free markets are able to continue investing capital productively.

In this new market regime, we keep talking about how we expect inflation to remain consistently higher than previously and, as a result, interest rates will need to be higher too. Alongside this, elevated levels of post-Covid government debt create a drag on economies which, in turn, can lead to broadly more volatile market returns.

In this blog, we assess the current state of this trinity of market influencers through the lens of our macro themes.

Persistent inflation

Inflation has been on a rollercoaster ride since the Covid pandemic, driven higher by labour misalignment and energy-price spikes following Russia’s invasion of Ukraine and the consequent need for energy-supply adjustments. There then followed a downward trend where the energy price effects fell away, only to be replaced by the legacy concerns over higher wage costs. Wage inflation, once entrenched, is always difficult to remove, especially when ageing demographics and spending patterns are creating high demand for labour at the same time as we are seeing a shortage of the right employees.

To control this scenario, central banks need to create an environment in which unemployment rises. Using interest rates to do this can be both blunt and slow. The latest US Employment Cost Index has reminded the market that wage inflation is not coming down; this is unsurprising, given that US employment remains strong and is yet to turn meaningfully. Against this economic backdrop, we believe the US central bank will remain careful not to remove the tight monetary policy too soon. With inflation creeping back up and thereby pushing interest-rate expectations higher again, the market has become anxious once more.

In a previous blog, ‘Market outlook: A case of déjà vu’, we suggested that this inflationary growth phase would follow the ‘Goldilocks’ market period (where the trinity of market indicators were in line) and that it would lead to market volatility. It appears that we may have now reached this phase.

Human capital

There is one of our important macro themes at play here: human capital (the change in the type and cost of labour). This theme identifies the change in demographics that causes the shortage of labour, as well as the possibility that companies need to find alternatives. In the previous market regime, labour was relatively cheap and had little influence on the cost of production. Now, with wage growth running at higher levels than inflation, it is expensive, and increases the incentive to invest capital in alternatives (artificial intelligence and robots).

Recent data suggests there is a gradual deterioration in labour hiring, and this will eventually remove the need for higher rates. For the next few months though, we suspect that markets will continue to fret over inflation, with a heightened focus on the level of interest rates and central bank comments.

Government debt

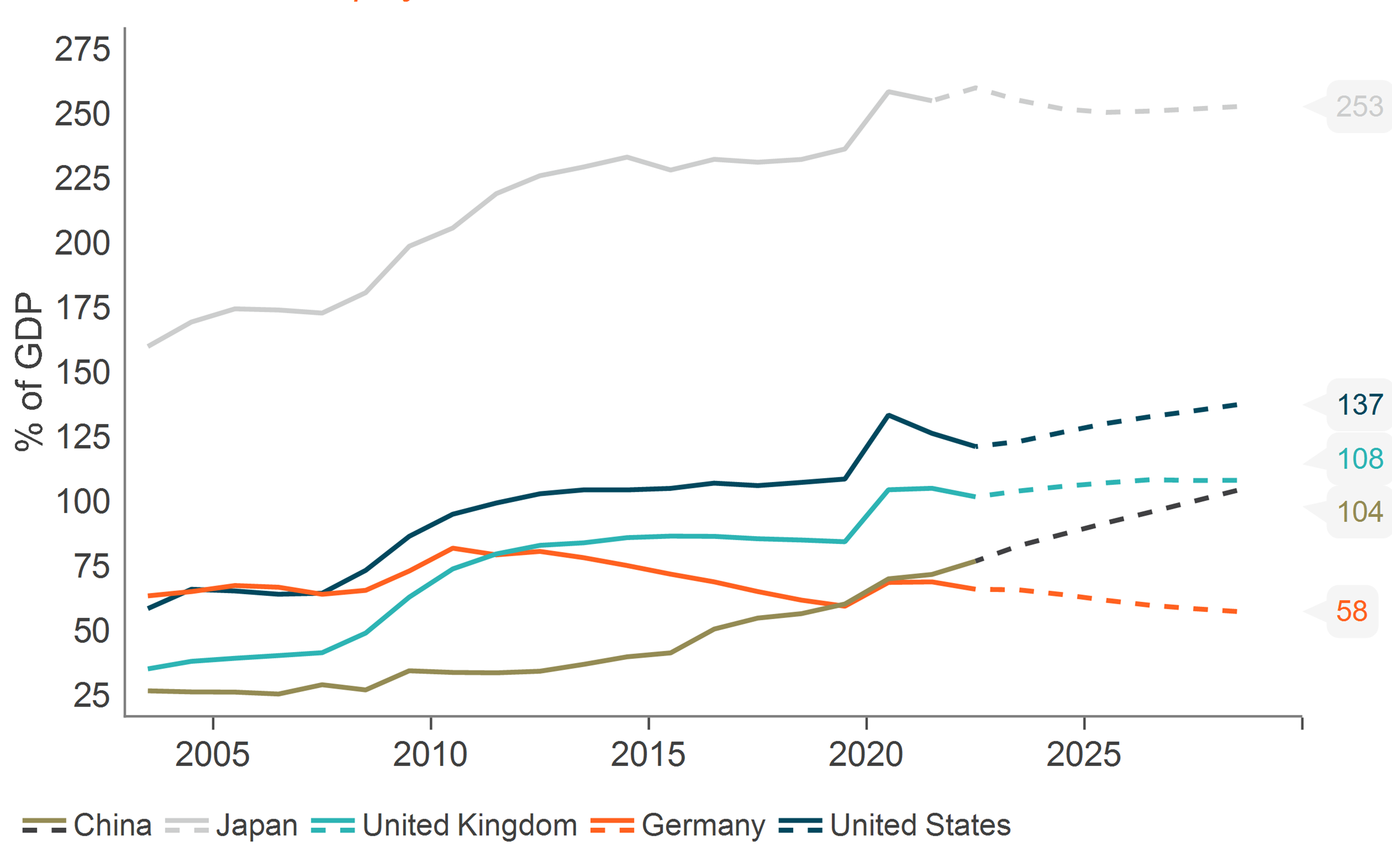

The third element of the market trinity, government debt, could prove to be important for the longer-term level of markets. Government debt levels have skyrocketed in recent years owing to the need to support the financial system after 2008 and the consumer during the pandemic. With government debt rising to levels not seen since the 1930s, and the cost of servicing that debt also on the rise, should we be concerned about the sustainability of that debt? We believe ‘yes’ is the answer, although there is always a ‘but’.

Our big government theme, which identifies the increased involvement of governments in the running of economies, concludes that high debt levels are here to stay. The post-Covid increase in social spending gave way to an increased focus on the need to be more self-sufficient in energy and supply lines.

General government debt trends for selected developed markets (% of GDP)

Source: Macrobond, International Monetary Fund data as of 5 April 2024

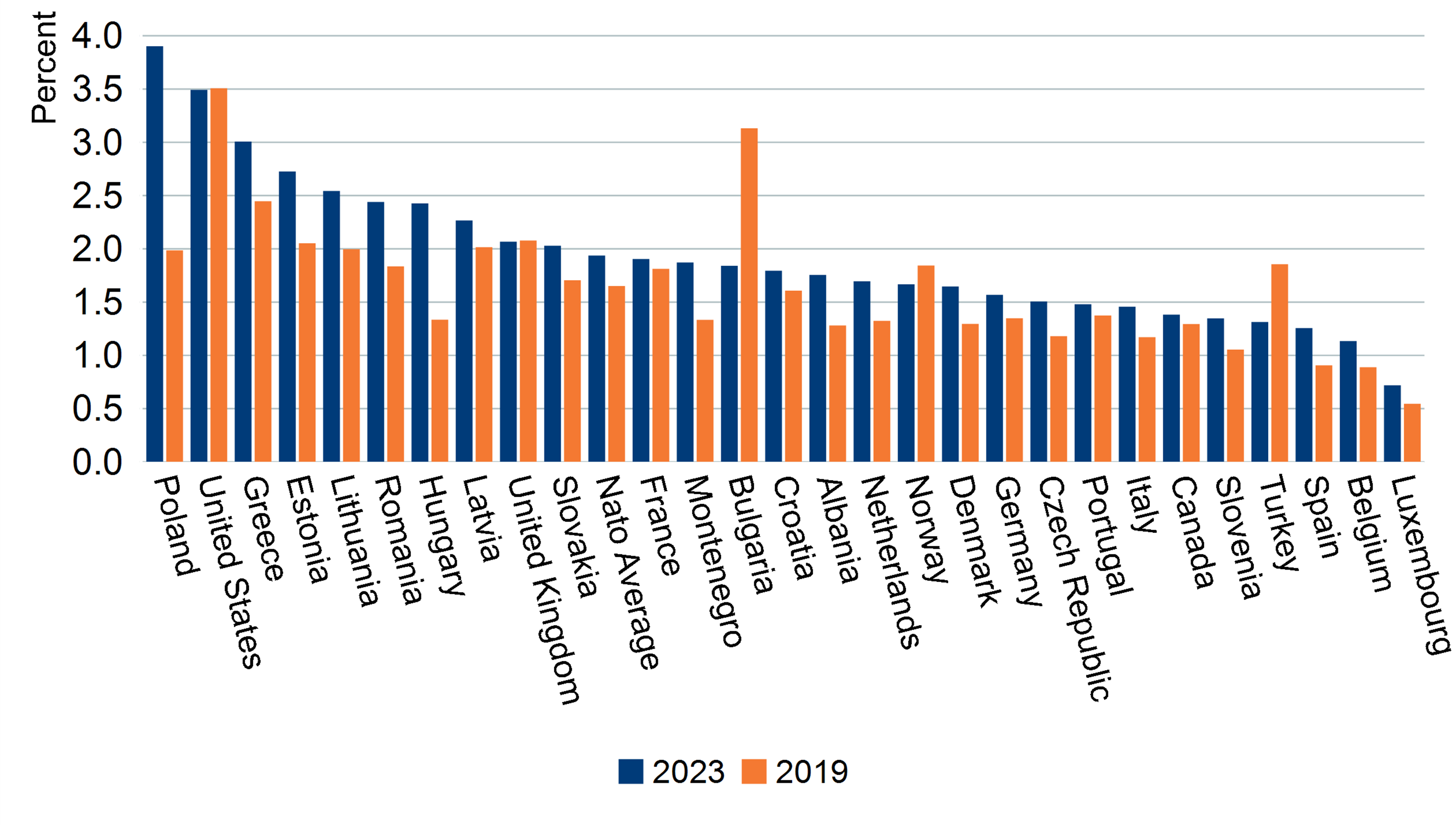

Furthermore, our geopolitical macro theme great power competition defines a period of heightened conflict resulting in a need for governments to increase defence spending. The chart below shows the change in defence spending for NATO members between 2019 and 2023 as a percentage of GDP.

NATO defence expenditure, % of GDP

Source: Macrobond and NATO, December 2023

Higher government debt levels may not be all bad news, however, as the offset to an increase in government debt is usually a reduction in private-sector debt. Taking the US as an example, since the 2008 global financial crisis we have seen a reduction in private-sector debt, particularly in financials (a direct response to the banking crisis) and households (which saw increased savings during the Covid pandemic).

Debt concerns

The concern for the market, though, is that the cost of debt keeps rising and, eventually, governments cannot afford the interest-rate bill. With bond yields set to remain higher for longer (reflecting the higher inflation story), this seems a legitimate concern. In addition, with governments needing to maintain spending on health and defence, the appetite for fiscal policy to support growth is undermined by the interest bill.

Less flexibility on spending plans can result in frequent political change, as successive governments fail to fulfil their electoral policies, and a potential crowding out of other investments. We believe fears might grow that the debt is unsustainable, and investors may start to worry about default.

In the past, high debt levels have been managed through financial repression (post global financial crisis) and by inflating the problem away. If inflation is high, nominal GDP grows rapidly and so too does tax revenue. Ultimately, the debt becomes more affordable. This appears to be the phase we are in now. Meanwhile, forcing domestic investors to buy the bonds issued by the governments is also an approach which allows the debt to find buyers while we wait for inflation to have an impact. In some countries (Japan, for example) this may be required to allow the central banks to stop their bond purchases.

Could calm return?

When the market trinity of inflation, debt and interest rates is on the rise, market anxiety rises, as does higher volatility. We believe we have entered this phase but there are early signs that calm can return. Tighter monetary policy is starting to influence employment, thus reducing the need to have higher wages. Unfortunately, it may take some time for headline inflation to resume its downward trend which, in turn, will allow central banks to reduce interest rates. Higher-for-longer inflation and interest rates can raise awareness of the cost of high government debt levels, which also keeps markets nervous. And yet here too, we can see some solutions further down the road. In an upcoming blog, we will delve more deeply into the potential for deflation to become the dominant theme later in the year.

Authors

This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This material is for professional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that holdings and positioning are subject to change without notice. Analysis of themes may vary depending on the type of security, investment rationale and investment strategy. Newton will make investment decisions that are not based on themes and may conclude that other attributes of an investment outweigh the thematic structure the security has been assigned to. MAR006265 Exp 06/2029

This material is for Australian wholesale clients only and is not intended for distribution to, nor should it be relied upon by, retail clients. This information has not been prepared to take into account the investment objectives, financial objectives or particular needs of any particular person. Before making an investment decision you should carefully consider, with or without the assistance of a financial adviser, whether such an investment strategy is appropriate in light of your particular investment needs, objectives and financial circumstances.

Newton Investment Management Limited is exempt from the requirement to hold an Australian financial services licence in respect of the financial services it provides to wholesale clients in Australia and is authorised and regulated by the Financial Conduct Authority of the UK under UK laws, which differ from Australian laws.

Newton Investment Management Limited (Newton) is authorised and regulated in the UK by the Financial Conduct Authority (FCA), 12 Endeavour Square, London, E20 1JN. Newton is providing financial services to wholesale clients in Australia in reliance on ASIC Corporations (Repeal and Transitional) Instrument 2016/396, a copy of which is on the website of the Australian Securities and Investments Commission, www.asic.gov.au. The instrument exempts entities that are authorised and regulated in the UK by the FCA, such as Newton, from the need to hold an Australian financial services license under the Corporations Act 2001 for certain financial services provided to Australian wholesale clients on certain conditions. Financial services provided by Newton are regulated by the FCA under the laws and regulatory requirements of the United Kingdom, which are different to the laws applying in Australia.

Comments