November 10 saw a fourth general election in four years for Spain’s voters. Barely six months on from the previous election in April, when Socialist (PSOE) caretaker Prime Minister Pedro Sanchez was unable to form a majority government to break the political deadlock, the country appears to be back in the same predicament. In the background, Catalonia has continued to polarize public opinion and create problems for the Madrid government, which have only recently been exacerbated by the jail sentences handed down to nine leaders of Catalonia’s independence movement. The ensuing mass civil unrest in the region has stretched the police force to capacity.

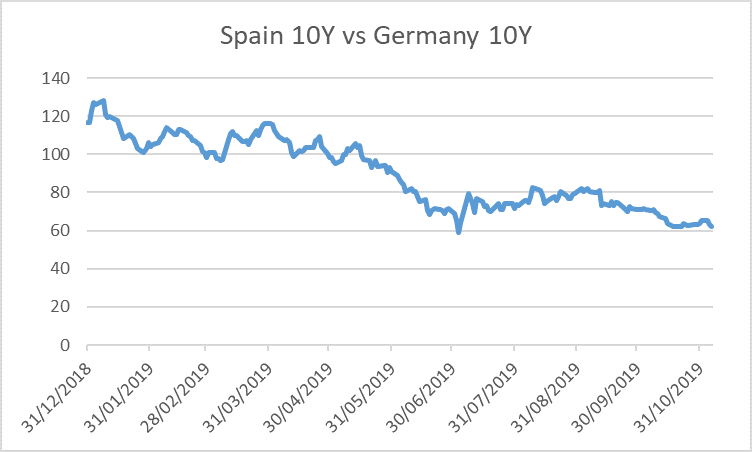

That being said, continuing political uncertainty, which has prevailed since last April’s election, has had little impact on Spain’s cost of borrowing. Spanish bonds have outperformed along with other peripheral European markets, primarily owing to the European Central Bank (ECB) increasing its loose monetary policy in response to economic weakness in northern Europe.

10-year Spreads on Spanish Versus German Government Debt (Basis Points)

Source: Bloomberg, November 6, 2019

Fragmented Politics

We have been talking about the gradual fragmentation of European politics as a longer-term trend. In the aftermath of the 2007-8 financial crisis, there has been a prolonged period characterized by low growth and rising wealth inequality. In this context, there has been a gradual shift away from the center ground of politics, with increasing votes for both left and right-wing political parties that have come to the electorate promising change.

Spain is a prime example of this, with many voters perceiving the established parties not only to have done a bad job, but also to be corrupt. Consequently, the established Spanish parties have lost votes as new parties have been created on a promise that they will fix things. First, we saw the creation of the left-wing Podemos party (now part of Unidas Podemos), which came to being on a ticket of radical change. Then the center-right Ciudadanos (Citizens) Party was formed, principally to fight corruption. Both these new parties have eroded votes from the old guard of the center-left PSOE and conservative Partido Popular (PP) parties: the more parties you have, the greater the chances of being unable to form a majority government. However, such developments have little impact on markets, as there is hardly any change in economic policy, especially in Europe, where monetary policy is set outside the country.

Change Agents

Unfortunately, the electorate remains dissatisfied and looks for further ‘change agents’, which leads to a second phase, which is an even greater shift to more extreme left and right-wing parties. Once again, Spain is a good example of this, as the results of the November 10 election now confirm. The ruling PSOE won 28% of the vote, 1% less than in April, while the Vox party (formed in December 2013), which had leapt into fifth place in the April 24 election, has done even better this time, moving up to third place, with 15% of the vote. There are different opinions on how right-wing Vox is, but clearly its Spanish nationalist policies are appealing to those who feel threatened not only by Catalan independence, but also by immigration. The center-right PP also grew its share of the vote to almost 21%

Electioneering Breeds Contempt

The party that has fared worst is the Citizens Party, which saw its share of the vote drop from almost 16% in April to less than 7% last Sunday. It is a good example of what can happen between phase one (new parties promising change) and phase two (even more extreme parties promising change). The Citizens Party is suffering from that well-known problem that if you promise change and then fail to deliver it, you just become part of the establishment and get the blame. The new failed parties do not have a group of core voters who would vote for them regardless of any political inaction, as they had appealed to a broad group of dissatisfied voters who move onto the next new bright shiny thing.

This has now come to pass in Spain once again, with the caretaker prime minister looking to forge a new coalition. Thus the political impasse remains in place, albeit with some new contestants coming to the fore.

Here we come across the other continuing trend, which is a little more subtle: constant electioneering with multiple party options can lead to arguments between parties, which makes it harder to form coalitions. Additionally, shifts to the extreme left and right make it challenging for parties to work together, owing to their differences on ideological grounds (witness the failure of the left-wing Five Star Movement and right-wing League coalition in Italy).

Shift Towards Increased Government Spending

It seems unlikely to us that the latest Spanish election will have a material effect on the value of the euro, as the single currency is driven by a pan-European economic outlook and the ECB’s interest-rate policy. Furthermore, the yield spread between Spain and its European neighbors is likely to be influenced by anything that changes either the credit quality and/or the degree of government-bond supply. With that in mind, we should remember that each European Union country is limited in the amount of debt it can issue; thus radical changes to fiscal policy seem unlikely. For example, populist Italian politicians talked frequently last year about increasing the country’s budget deficit, but then found themselves constrained.

Nonetheless, we note the growing trend within Europe, as elsewhere, to provide economic support through increased government spending. With economic growth generally weak across Europe, and monetary policy at an extreme, we anticipate a continued shift towards more fiscal intervention. At the same time, with the environment rising up the political agenda, we wonder how long it will be before we see government borrowing being channeled into renewables and greater energy efficiency.

Authors

Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice.

Important information

US - Text disclosure - NIM

This is a financial promotion. Issued by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Newton Investment Management Limited is authorized and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. 'Newton' and/or 'Newton Investment Management' brand refers to Newton Investment Management Limited. Newton is registered in England No. 01371973. VAT registration number GB: 577 7181 95. Newton is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940. Newton's investment business is described in Form ADV, Part 1 and 2, which can be obtained from the SEC.gov website or obtained upon request. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. You should consult your advisor to determine whether any particular investment strategy is appropriate. This material is for institutional investors only.

Personnel of certain of our BNY Mellon affiliates may act as: (i) registered representatives of BNY Mellon Securities Corporation (in its capacity as a registered broker-dealer) to offer securities, (ii) officers of the Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds, and (iii) Associated Persons of BNY Mellon Securities Corporation (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Mellon Investment Management firms, including Newton and (iv) representatives of Newton Americas, a Division of BNY Mellon Securities Corporation, U.S. Distributor of Newton Investment Management Limited.

Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any governmental entity) and are not guaranteed by or obligations of The Bank of New York or any of its affiliates. The Bank of New York assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection therewith. © 2020 The Bank of New York Company, Inc. All rights reserved.