Strategy Profile

-

Objective

-

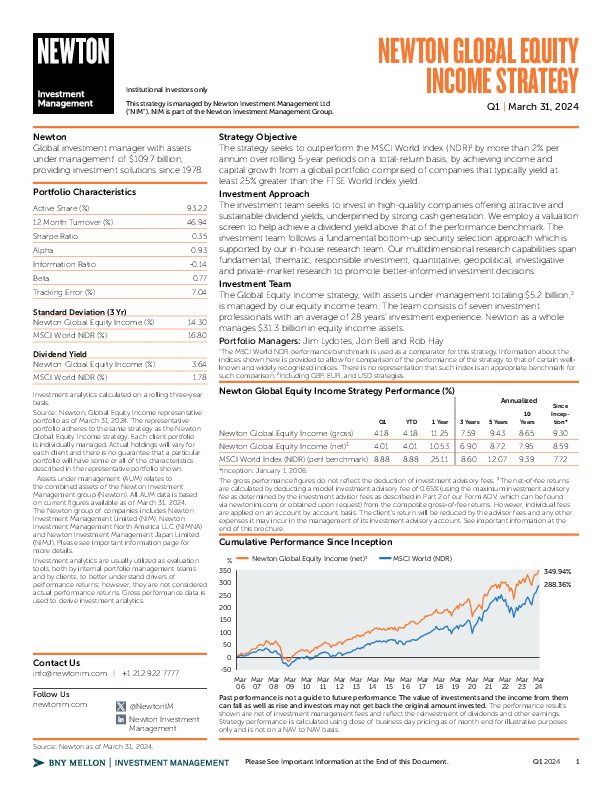

The strategy seeks to outperform the MSCI World NDR Index by more than 2% per annum over rolling 5-year periods on a total-return basis, by achieving income and capital growth from a global portfolio comprised of companies that typically yield at least 25% greater than the FTSE World Index yield.

-

Performance benchmark

-

MSCI World NDR Index (total return), FTSE World Index (yield criteria)

-

Typical number of equity holdings

-

40 to 70

-

Yield discipline

- Every new holding in a global equity income portfolio typically has a prospective yield 25% greater than the benchmark at the point of purchase. Any holding whose prospective yield falls below the benchmark yield will trigger our sale discipline process.

-

Strategy inception

-

January 1, 2006

Quarterly factsheet

Facts on the strategy’s performance and positioning.

Investment Team

-

-

Our Global Equity Income strategy is managed by our equity income team. In-house research analysts are at the core of our investment process, and our multidimensional research platform spans fundamental, thematic, responsible investment, quantitative, geopolitical, investigative and private-market research to promote better-informed investment decisions.

Meet the Managers

Want to find out more?

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

ESG can be one of many inputs into the fundamental analysis. Newton will make investment decisions that are not based solely on ESG analysis. Other attributes of an investment may outweigh ESG analysis when making investment decisions. The way that material ESG analysis is assessed may vary depending on the asset class and strategy involved. As of September 2022, the equity investment team performs ESG analysis on equity securities prior to their recommendation. ESG analysis is not performed for all fixed-income securities. The portfolio managers may purchase equity securities that are not formally recommended and for which ESG analysis has not been performed.