The current macro environment and promising sector fundamentals bode well for US value stocks.

As stocks continue their volatile ride in 2022, investors are searching for a smoother path to attractive returns. In our view, US value stocks are a compelling opportunity that may retain their current leadership role in a less certain market backdrop. After ten years of well-publicized underperformance, value stocks’ rebound over the last 18 months, particularly relative to growth stocks, is noteworthy.

The intensity of rising inflation and the ensuing higher interest rates portend a favorable environment for value stocks, which should provide a tailwind for the trend to continue. Higher rates tend to weigh on growth stocks as cash flows that are anticipated well into the future end up with a lower present value. Conversely, value stocks possess “short-duration” asset characteristics as they tend to realize their cash flows sooner.

Furthermore, at the sector level we find areas where a combination of attractive valuation metrics and evolving industry trends offer opportunities for stock picking. In particular, we like certain industries in the Financials and Industrials sectors.

We believe there is still great value in value investing.

Value Renaissance

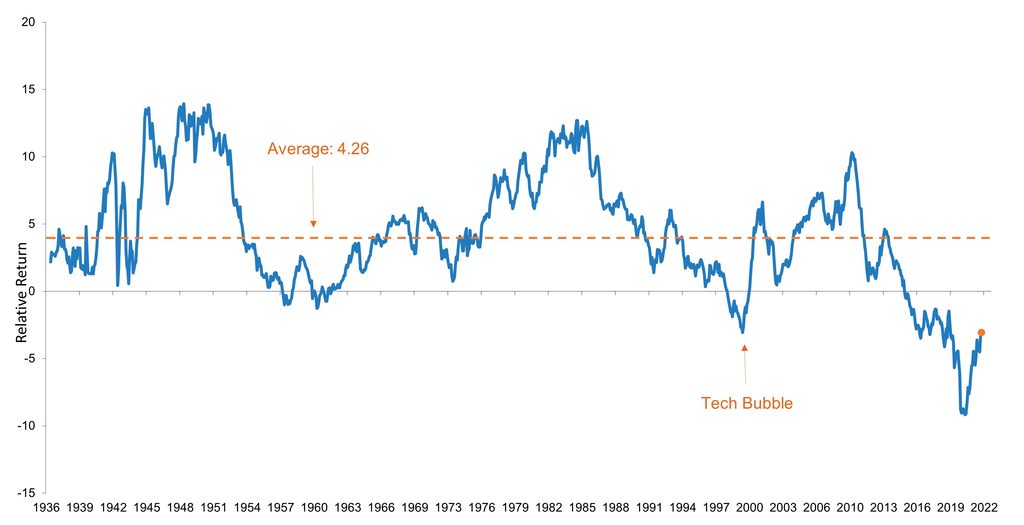

A long-term view of the relationship between value and growth offers perspective. The chart below plots the long-term performance history of US value versus growth, with the dotted green line the average outperformance of value over rolling 10-year periods back to the Great Depression. The far-right side of the chart shows just how early we look to be in the cycle for value leadership, and just how extreme the growth outperformance has been.

Value/Growth 10-Year Rolling Relative Return

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. For illustrative purposes only. Source: Alliance Bernstein, as of February 2022.

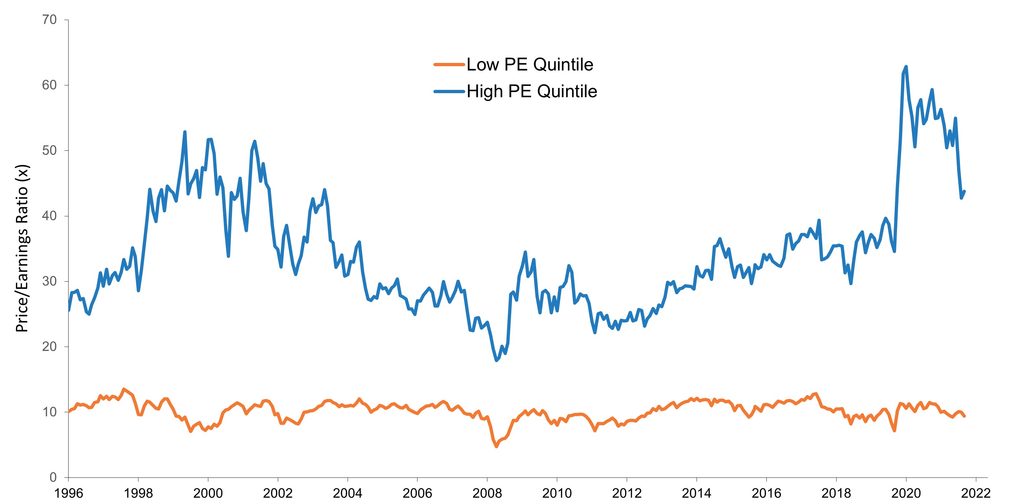

The next chart illustrates the historical spread in valuations between the cheapest quintile and most expensive quintile of the market—a proxy for growth versus value. Again, the far-right side of the chart shows how extreme the spread had become during Covid, which was the widest over the last 25 years. While the valuation spread has narrowed during the recovery, it remains at a historically attractive level.

S&P 500 P/E Valuation levels: Low (Cheap) vs. High (Expensive) Quintiles (8/31/1996 – 3/31/2022)

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Source: Bloomberg, FactSet as of 3/31/22.

Favorable Valuations

What we find unique about the current environment is that higher rates and more persistent inflation seem to be the consensus, yet this outlook has not trickled down to the valuation profile of the market segments most likely to benefit. So, despite the uncertain economic outlook, we are identifying compelling value opportunities, even within more economically sensitive sectors such as Financials and Industrials.

Financials

The Financials sector has long been a beneficiary of higher rates and inflation; we believe the group is poised for resilience as the capital profile of US banks remains robust. Notably, the sector is also offering the most attractive valuations in decades.

Financials Relative Price-to-Book Ratio: 1952 – March 2022

For illustrative purposes only. Drawn from the largest 1,500 stocks; capitalization-weighted data. Source: Corporate Reports, Empirical Research Partners Analysis.

Currently, banks and diversified financials are exhibiting strong balance sheets and capital ratios, in stark contrast to the period during and after the global financial crisis (GFC). Furthermore, over the course of the Covid-19 pandemic, banks and diversified financials passed the US Federal Reserve’s (the Fed) stress tests, which included dire US unemployment assumptions of 15-20%. Another advantage between the current potential recessionary environment and the former GFC is the more stringent current expected credit loss (CECL) accounting standards. These rules went into effect in 2020 and are very conservative, requiring banks to provide for loss assumptions over the life of a loan immediately.

Finally, despite a slowing economic outlook, we believe loan demand can improve for the banks. As rates rise and liquidity is removed from the system, money is no longer “free,” forcing borrowers to pivot toward traditional banks and away from non-bank alternatives. We haven’t seen a meaningful corporate credit expansion in this cycle, and there are several areas within the energy transition theme that will require capital regardless of the economic environment.

Outside of banks and diversified financials, the insurance segment also offers attractive opportunities against a volatile, inflationary backdrop. The group is typically less volatile than the overall Financials sector as products are generally non-discretionary in nature. Additionally, idiosyncratic opportunities abound in life, non-life and specialty insurers as select companies seek to dispose legacy businesses with higher rate or market sensitivity, and redeploy capital into higher-margin, lower-capital intensity fee-based business.

Industrials

We have also found pockets of opportunity within Industrials, primarily in capital goods and aerospace & defense. We believe capital goods companies that will benefit from an accelerating US capital-expenditure cycle will be of interest to investors as the persistent underinvestment in our physical infrastructure stimulates action. The chart below details the concerning result of “kicking the can down the road”:

Average Age of Private Fixed Assets

Source: Bureau of Economic Analysis, as of August 19, 2021.

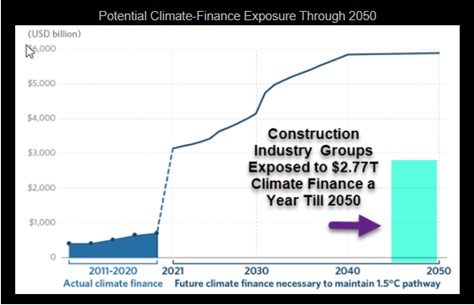

The broader energy transition theme, which encompasses trends within electrification and warehouse automation, among others, is supportive of idiosyncratic opportunities within the sector. Companies with exposure to construction spending from the Utilities and Telecommunication Services sectors are poised to benefit even in a more unsettled economic environment.

Source: Climate Policy Initiative and Bloomberg Intelligence, as of November 2, 2021.

Finally, large-scale spending intentions, such as the US infrastructure plan, underpin GDP-agnostic demand conditions within the broader capital goods space.

The aerospace and defense segment also offers areas of potential as global defense budgets, particular in the US and Europe, rise as a result of Russia’s continued invasion of Ukraine. Concurrently, commercial aerospace trends are continuing to improve with broader volume recovery in the airline industry, and opportunities driven by strong airliner aftermarket activity could persist even in a weaker economic backdrop.

Still Finding Value in Value

We believe that value-oriented securities that exhibit solid earnings momentum over the coming quarters remain poised to outperform the market. Realistically, we expect that above-trend inflationary pressures and supply chain issues will create roadblocks for certain industries, and risks remain. Looking ahead, we will continue to focus on companies that exhibit valuation protection, current earnings, and cash flows that can beat expectations and pricing power in an inflationary environment. As always, we continue to look for periods of near-term volatility to identify attractive relative value opportunities.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY Mellon"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.

Comments