Key Points

- Trend-following strategies measure market sentiment by analyzing recent historical returns.

- In our view, these strategies can be incredibly diversifying for investor portfolios owing to their low correlation to stock prices.

- While conventional trend following can be additive, we believe that the traditional recipe can be improved upon through the optimization of signal processing.

Only one kind of ‘alternative’ strategy did well in 2022: ‘trend following’ or ‘managed futures,’ which capture broad patterns of market sentiment, both bullish and bearish. In fact, some managed futures strategies were up over 70% last year.1

What Is Trend Following?

Trend-following strategies measure market sentiment by analyzing recent historical returns. Many consider the process to follow the tenets of human psychology. For example, if a portfolio was heavily underperforming last week, would an investor feel bullish or bearish this week? Most investors would probably feel bearish, and it turns out that, more often than not, this psychology can lead markets to continue their recent trajectory. Trends tend to be most persistent during times of significant market or economic upheaval, frequently when multiple asset classes are performing poorly. Consequently, trend following typically has its best opportunities when other investments are faltering.

In our view, trend-following strategies can be incredibly diversifying for investor portfolios. Historically, they have had zero, or even negative, correlation to stock prices—virtually no other easily accessible return stream has that characteristic. Additionally, trend following tends to do best in environments that are unfavorable for the balance of investor portfolios. From our perspective, this makes it an effective diversification tool for investors.

Improving on Conventional Trend-Following Methodology

While conventional trend following can be additive, we believe that the traditional recipe can be improved upon through the optimization of signal processing by harnessing related-market information, disaggregating security-specific information from asset-class information, accounting for mean reversion in over-extended trends, and only investing where and when trends are found.

Concept 1: Harness Information from Related Markets

Conventional trend-following strategies use the historical performance of a market to predict its future behavior. For example, individual markets like West Texas Intermediate (WTI) crude oil, S&P500® futures or US 10-year Treasury futures are each used to predict their own future direction, ignoring the historical behavior of closely related markets like Brent crude oil, Russell 2000 or 10-year UK gilt futures.

In our view, a more nuanced approach incorporates information from related markets to predict future direction. For example, if there are five markets that are closely related to WTI crude oil, it could be more advantageous to include information from all of them to predict the future behavior of WTI. This process creates the ability to look for common signals across a group of markets to predict the future direction of WTI. Ultimately, this approach enables the identification of more signal per unit of noise.

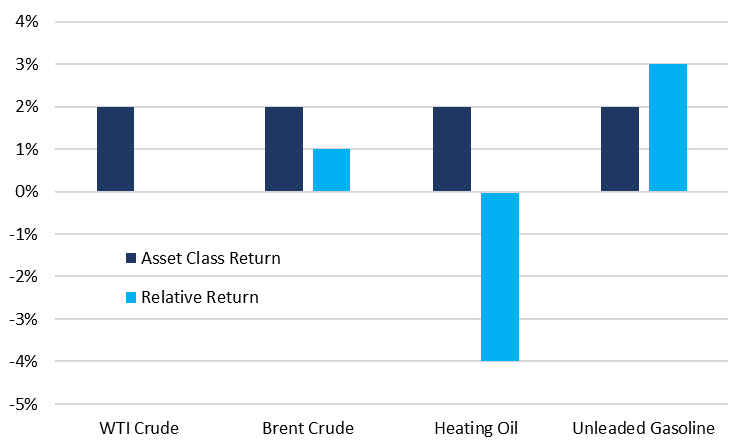

Concept 2: Disaggregate Market Returns with Different Time Horizons

Recent returns from a set of related markets can provide information about asset class momentum as well as relative price momentum within the related markets. Asset class momentum and relative price momentum have opposite implications for future return when using shorter-term signals.

This information needs to be disaggregated to properly predict future market direction. As noted in the graphs below, we provide a theoretical example to disaggregate security-specific information from asset class information and model the time series behavior of each separately.

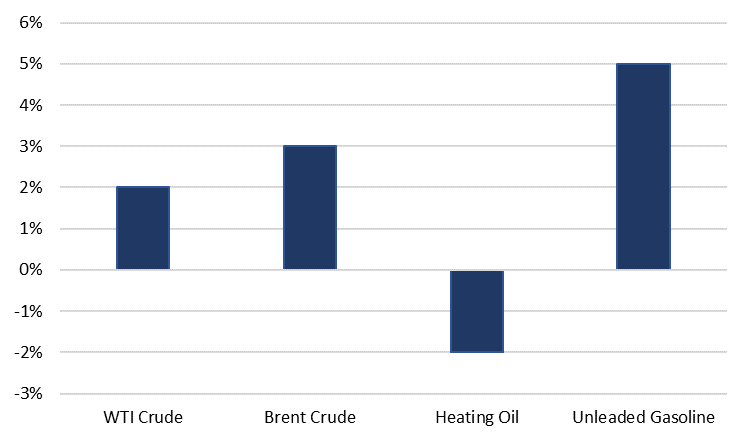

Recent Market Return

Source: Newton, for illustrative purposes.

Disaggregated Market Return

Source: Newton, for illustrative purposes.

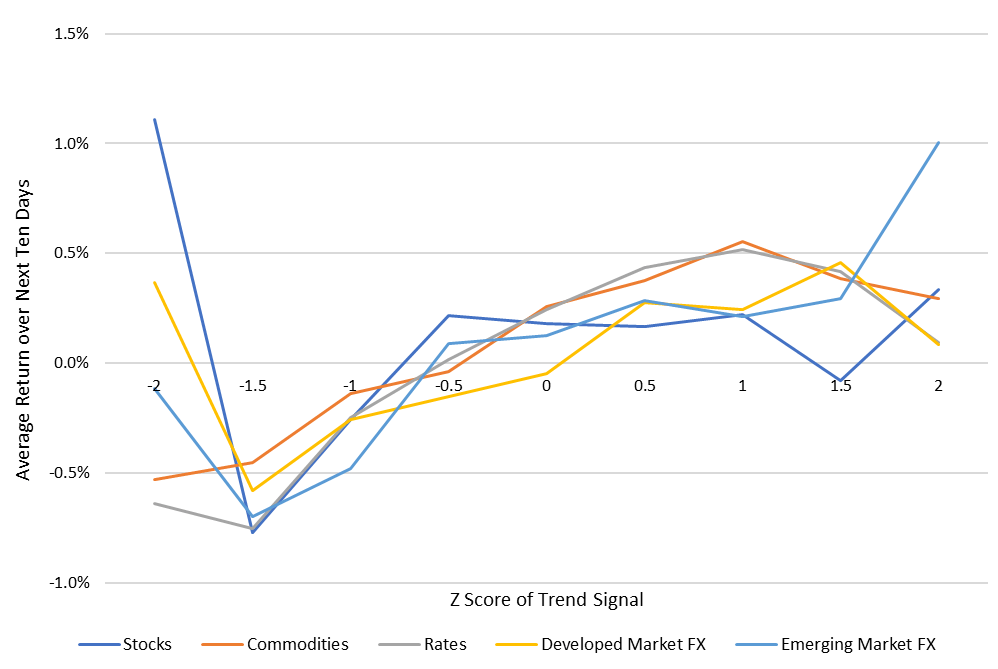

Concept 3: Mean Reversion in Over-Extended Trends

As a trend signal strengthens, the likelihood that it is caused by market noise falls, increasing the optimal position size in the trend.

At the same time, stronger trend signals are associated with larger recent moves, and large moves tend to predict future moves in the opposite direction. This argues for an optimal position that gets smaller when signals cross a specified threshold.

These opposing forces can make investing in short-term trends challenging. To solve this, we model these two dynamics separately, then combine them into an optimal position size.

Extreme Trend Signals Can Mislead

Source: Newton, for illustrative purposes.

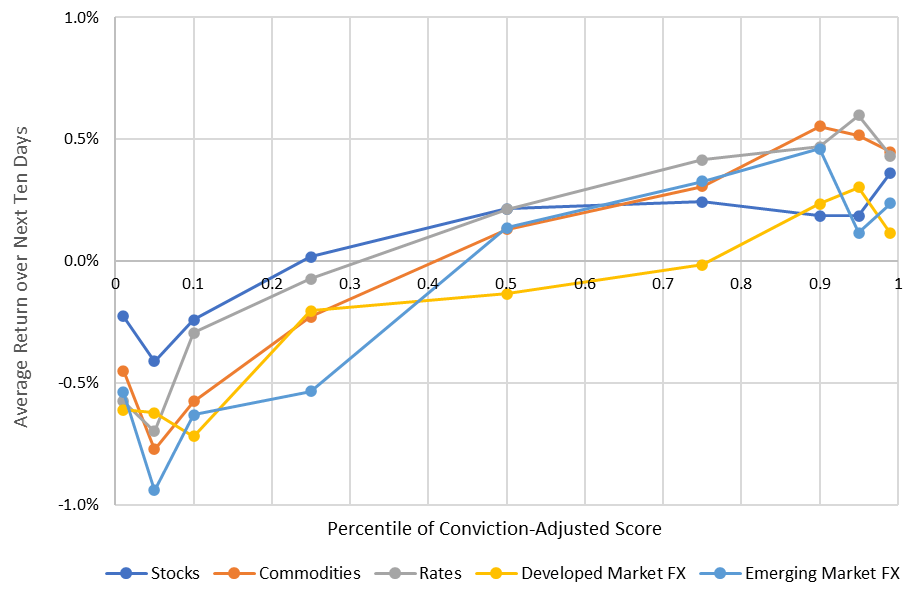

Reversion-Adjusted Signals Improve Forecasting

Source: Newton, for illustrative purposes.

Concept 4: Only Invest Where and When There Are Trends

Videos

Many trend-following strategies employ a similar amount of risk at all times and allocate the same amount of risk to each asset class, regardless of the relative prevalence of trending opportunities. We believe a more thoughtful approach to signal-processing techniques can make signals even more informative. By concentrating the amount of risk based on where and when outsized signals are found, substantial risk may be avoided in markets where there is little evidence of trends.

Conclusion

In 2022, strong trends arose as the prices of stocks and bonds tumbled. In 2021, commodities rallied powerfully. In late 2020, the Covid pandemic buoyed several asset classes. In 2014, commodities were the winners of the day. In 2008 during the global financial crisis, most risk assets were halved. These time periods illustrate that market upheaval happens frequently, and a strategy that thrives in the most challenging environments can be particularly valuable in such instances. Furthermore, we believe conventional trend-following strategies can be improved upon through several optimization concepts, allowing investors access to what we believe is a highly valuable diversification tool.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY Mellon"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.