Key Points

- We believe there is a significant sector dislocation in US utilities, potentially unlocking opportunity for active managers.

- Government incentives aimed at decarbonization can provide tailwinds for renewables-exposed utilities.

- We believe electrification and investments in energy independence may continue to drive US electric and gas utilities.

Investing within the utilities space has long been a choice between the US or Europe, with varying positive and negative aspects to each locale depending on the current regulatory environment. In particular, government intervention has traditionally been a key concern for investors in European utilities. Historically, when energy prices spiked in Europe, governments and regulators protected the consumer by dampening heating and electrification prices. This consumer protection has come at the expense of utilities companies, hurting their bottom lines and making them less attractive from an investment perspective.

European Utilities Have Dominated Since 2022

During the first few months of 2022, European energy prices began to surge after the start of the Russian/Ukrainian conflict raised concerns that Russia would turn off its natural gas supply to the rest of Europe. Investors largely assumed that governments and regulators would once again step in to cap prices for consumers and thereby reduce profits for utility companies. With this expectation, European utility companies largely underperformed during the first half of 2022.

At the time, our view toward European utilities was opportunistic. We found attractive valuations in the space, particularly relative to US utilities. Additionally, it was our belief that governments and regulators would again seek to help consumers but not to the extent they had previously. Instead, we thought that regulators would temper their impact on European utility companies as they recognized that utilities needed additional capital to allocate to renewables projects. These renewables programs are key for many countries that fear overreliance on Russian energy and seek to enhance their own energy output.

Our belief in a more favorable-than-expected environment for European utilities was largely accurate. Governments were supportive of the utility sector and European utilities subsequently enjoyed a robust recovery.

Where Are We Now?

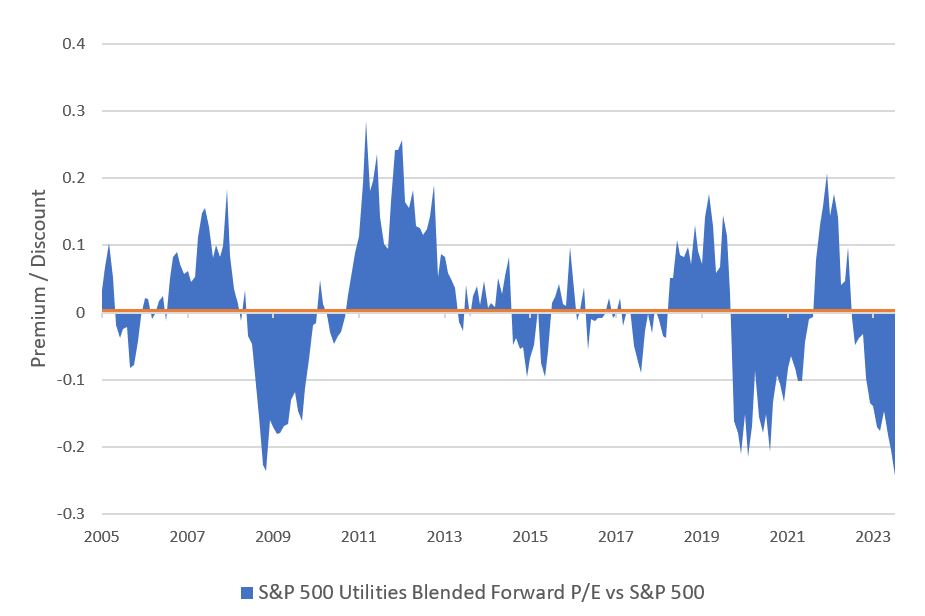

While European utility companies have produced robust returns, US utilities were one of the hardest-hit areas in 2023. As borrowing costs creeped higher, many US renewable projects became uneconomic and US utilities became quite volatile. We believe this has created a large dislocation between utilities and other sectors. As shown below, as of early February 2024, US utilities traded at their largest discount to the S&P 500® (blended forward price/earnings (P/E) ratio) in at least 19 years.

However, now new regulations in support of renewables projects have come into effect across almost all 50 states. Currently, there are 23 states in the US with 100% clean-energy goals, representing 53% of the US population.[1] Regulators understand that, in order to hit these ambitious targets, they need to help adjust the economics of utility companies, enabling continued investment in renewables projects. US utilities should continue to benefit as the incentives created by the Inflation Reduction Act accrue in the coming years, especially in areas such as wind and solar that can take years to develop from planning to completion. We believe US utility companies will not only benefit from the new renewables regulations, a critical area within the long-term decarbonization theme, but also from the deglobalization initiated after the Covid pandemic and rising geopolitical tensions as nations seek to better control their supply chains and sources of energy. We believe that the continuation of this US investment is crucial to ensure energy independence in an environment of growing electricity demand stemming from the energy transition.

Conclusion

Given the thematic tailwinds, government support and growing demand for electricity and renewables, we believe US utility companies are well positioned to create value. As US utilities experience attractive valuations, and as regulators begin to provide positive incentives for renewable projects, we believe that US utilities could see a rerating. In our view, the wind is blowing west, and US utilities should begin to see the fruits of the current regulatory environment.

[1] https://www.cesa.org/projects/100-clean-energy-collaborative/guide/table-of-100-clean-energy-states/

Authors

James A Lydotes

Head of equity income and deputy chief investment officer, equity

Brian Blongastainer

Global investment strategist

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR005827 Exp 02/29. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY Mellon"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.