Easing supply-chain pressures and rapid innovation should revitalize the mobility theme.

Key Points

- Technology stocks faced numerous challenges in 2022—principally rising rates and slowing growth—after several years of solid fundamentals and returns.

- Supply-chain and logistical challenges that emerged during the Covid pandemic have affected the key drivers of the mobility theme, though backlogs are expected to ease with help from easing regulations and improved transparency.

- While higher interest rates are likely to affect automobile sales, we expect the growth of electric vehicles (EVs) to continue as new models are launched at attractive price points and government incentives remain in place.

- The development and deployment of Advanced Driver Assistance Systems (ADAS) continues to make new vehicles safer, and ADAS are likely to accelerate the development of scalable autonomous vehicles.

Macro Outlook

With investors saying goodbye to 2022 and cautiously welcoming 2023, from our perspective success in the new year could center around a significant list of concerns. First and foremost are interest rates. After a decade and a half of “free money” through central bank quantitative-easing programs, investors find themselves in unfamiliar territory—normalizing interest rates. The US Federal Reserve (Fed) is leading the way with an unapologetic and staunch focus on combating “persistent” inflation that seems to be well entrenched. We believe that the longer inflation persists, the more likely it is to become self-sustaining, which is why the Fed appears so determined. Many sectors continue to experience supply-demand issues as global supply chains have yet to fully recover from the Covid-19 pandemic. In addition, demand remains buoyed by robust household and business balance sheets sustained by pandemic-era stimulus. Adding to this pressure is the stubbornly strong employment rate evidenced by an incredibly tight US labor market. Reduced labor-force participation has already taken its toll on lower-paying industries—the leisure and hospitality sector has seen the highest quit rate since July 2021, and retail does not appear far behind according to the US Chamber of Commerce. Many areas of the US economy are struggling with a shortage of skilled workers, including wholesale and retail trade, education, and health services, pressuring current employees who are likely to be facing longer hours, increased responsibilities and fatigue. The American Enterprise Institute’s Nicholas Eberstadt, writing in the Washington Post, suggested that “The US labor shortage will probably have to be solved by some combination of immigration, automation and recession.”

The geopolitical landscape, and the war in Ukraine in particular, has also contributed to inflation. Given the heavy sanctions on Russia, as well as Russia’s blockade to Ukraine shipping, we believe there is potential for a surge in energy and food prices. In addition to the Ukrainian invasion, North Korea continues its saber-rattling while mainland China threatens Taiwan and asserts dominance over Hong Kong. These destabilizing developments continue to force investors to contend with increasing macro variables that may influence markets regardless of fundamentals, and impact global trade.

In our opinion, signs of a global recession are building as well, evidenced by the Global Composite Purchasing Managers’ Index (PMI) falling to 48 in November for the first time since the Covid-induced recession in early 2020. As a reminder, a level below 50 indicates contraction. We believe the US economy is facing a similar dilemma. In November, the US Composite PMI level fell to 46.4. In addition, we believe services prices are cooling while gasoline prices recently fell to their lowest level in a year, indicating a slowing economy.

One remaining headwind is corporate earnings growth, which we believe is likely to decelerate in 2023. A slowdown in economic activity, which is expected globally, could translate into lower revenues and higher margin pressure, impacting earnings expectations to the downside for at for potentially the first half of the year.

That said, we believe a hard landing recession scenario remains a distinct risk, although unlikely. Capital expenditures in the US have remained robust and holiday sales numbers have surprised to the upside. Wage growth and employment have remained solid, helping to stave off recession talk, but this is likely to slow as higher interest rates work their way through the economy. As we progress further into 2023, in our opinion, equities could find some footing if the Fed nears its “mission accomplished” conclusion (lower/no more rate hikes), but, of course, that remains unknown.

Technology Outlook

Technology stocks faced numerous challenges in 2022—principally rising rates and slowing growth—after several years of solid fundamentals and returns. Rising rates drove particular weakness in the IT services and software industries. Semiconductor-related stocks declined due to slowing macro growth and now appear to be in a downcycle. Electronic equipment and instrument stocks were the most resilient companies in the sector. These stocks continue to see rising estimates as supply-chain conditions improve, enabling these companies to ship against backlogs that are at historically high levels.

Looking into 2023, fundamentals may remain mixed due to cyclical concerns, but remain positive on a longer-term secular basis. After facing strong demand during the pandemic, the semiconductor group is in a corrective phase as earnings estimates decline along with lower global consumer confidence. However, mobility-centric semiconductor company fundamentals are supported by more resilient demand, structural growth in content and increased pricing power due to strong innovation. While these companies may not be fully immune to the downtrend, below-average inventory levels and more attractive valuations provide some support as the cycle seeks to find a bottom in the first half of 2023.

Like semiconductors, software stocks are also in a corrective phase as rising rates, slowing sales cycles and a strong US dollar weigh on fundamentals. Software is increasingly fundamental to the mobility theme as it plays a role in processing, automating, and securing an increasing array of mobility applications. According to an Irish-American automotive technology supplier, “software-defined vehicle” is a term that describes a vehicle whose features and functions are primarily enabled through software, a result of the continuing transformation of the automobile from hardware-based to a software-centric electronic device on wheels. Premium vehicles today can have up to 150 million lines of software code, distributed among as many as 100 electronic control units and a growing array of sensors, cameras, radar and light detection, and light detection and ranging (lidar) devices. Mass-market vehicles are not far behind. Three powerful trends—electrification, automation and connectivity—are reshaping customer expectations and increasingly driving manufacturers to software solutions.

As we look to 2023, valuations are nearing longer-term average support levels while strong materiality to the theme and high levels of innovation underpin long-term growth potential. We expect new opportunities will unfold in 2023 once expectations reset in the first half.

Connectivity

5G and Mobile Networks

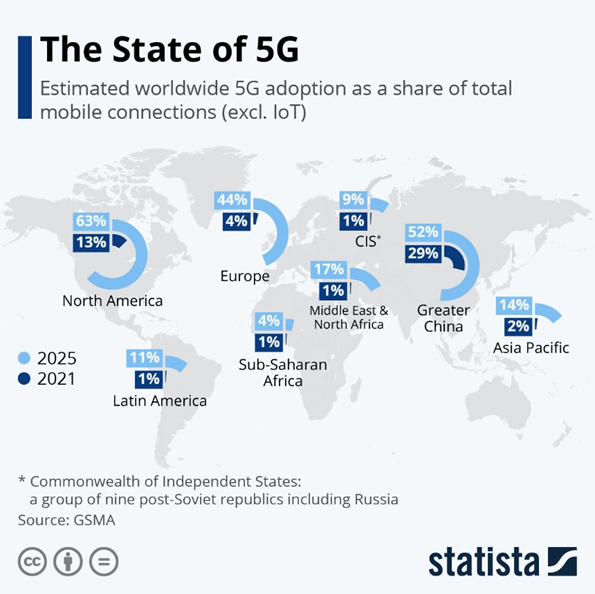

Connectivity continues to expand and transform many aspects of our life. The impacts of “work from home” have revolutionized our work/life balance by producing a permanent shift to a more balanced paradigm and enabled access to labor more broadly than ever. It is likely to be the new way of working and employers are embracing digital transformation and new connectivity tools to communicate, collaborate and manage their businesses with greater agility during this uncertain business climate. Globally, 5G is likely to continue to ramp up aggressively, which could usher in a host of new services and create new markets.

Why does the 5G rollout matter? It plays a critical role in a company’s ability to harness its high-speed, ultra-low latency, higher reliability, and massive network capacity to capitalize on services and technological capabilities never before available. For instance, auto original equipment manufacturers (OEM) and component suppliers can revolutionize their legacy businesses. Instead of a development cycle focused on “model years,” continuous software development may be driven by agile practices where OEMs will be able to deploy both new software and upgrades to a vehicle while it is parked in customers’ driveways or garages.

Supply Chains/Logistics

As we have discussed for some time, supply chains are evolving with greater end-to-end transparency that allows for more informed participant decisions. Whether a parts supplier tracks inventory sales, a distributor assesses real-time transportation needs, a merchant needs to understand if there are over/under supplies of goods to make pricing and inventory adjustments, or a consumer is tracking a package in near real-time to anticipate its delivery date, insights into supply chains should help drive long-term success.

Supply-chain management and logistics are benefiting from the convergence of technologies. With smartphones putting a computer in everyone’s hands, 5G broadens the reach, dramatically reduces latency while increasing reliability, power, and data speeds. Blockchain serves as a system of record and documentation. Sensor technology scans the automated labelling (bar codes, etc.) of packaging in distribution centers which ties directly into cloud-based inventory/enterprise resource planning systems, robotics, and automation technologies. Coupled with artificial intelligence/machine learning, these technologies boost efficiency by significantly reducing the picking, packing, and processing steps through higher levels of automation. These process and infrastructure improvements are also compounded by efficiency gains in last-mile delivery systems. Drones, electric vertical take-off and landing aircraft and commercial vehicles could redefine how logistics systems function, both through more efficient and autonomous route decision making and from more capable powertrains like electric vehicle (EV) and hydrogen fuel cells. Ultimately, improved insights from real-time inventory management will not only reduce emissions but also accelerate the velocity of the supply chain by raising inventory turns and improving customer satisfaction with reduced delivery friction.

Automobiles

Global auto production witnessed a continued recovery in 2022, but it was slower than what we expected a year ago due to supply-chain headwinds and logistical challenges. Looking ahead to 2023, the recovery should continue, but we believe the pace will remain slow and have periods of volatility depending on the manufacturers. Production divergence can be region-specific owing to continuing shortages of semiconductor supplies and other supply-chain disruptions. The restocking pace of inventories around the globe will depend on the supply chain.

In terms of our expectations for overall vehicle demand in the retail channels, we see higher global interest rates negatively affecting affordability, which can lead to deteriorations in price/mix in certain areas of the market. The lower purchasing power can affect the mass-market-priced models from OEMs the most, where the consumer is more sensitive to higher financing costs, while premium OEMs should be relatively less affected as buyers are typically in a better position to deal with increasing costs.

That said, because annual volumes in many regions like the US and Europe remain below pre-Covid levels, there is pent-up demand, while in China the outlook looks set to improve following the relaxation of the government’s zero-Covid policies. In the US, the seasonally adjusted annual rate (SAAR) bottomed in September 2021 at 12.7 million vehicles and rebounded to 15.4 million in October 2022. This is nowhere near the previous US SAAR levels of about 18 million. The Chinese market has been volatile in 2022, with some months that were robust and some months that were weak. Assuming China’s reopening continues, auto volumes should be positive, especially for new energy vehicles (NEVs) that are attractive to consumers. Outside of China, we expect the growth of EVs to continue in Europe and the US as more models are launched at more attractive price points and government incentives remain in place to make up for the cost difference versus comparable internal combustion engine models. In Japan, the market will continue to be slow to adopt EVs in our view, as policies have lagged other regions that are more focused on EVs. The EV market in India has been robust for two-wheelers, such as electric battery-powered scooters. Although passenger-vehicle EVs should grow, we believe the penetration will be low due to lack of models, affordability, and infrastructure.

Autonomous Vehicles

In 2022, we continued to see progression in the development and deployment of Advanced Driver Assistance Systems (ADAS) and full autonomous driving. Regarding the latter, in March 2022 a prominent Silicon Valley firm offered paid robotaxi rides to employees in San Francisco, and more recently received a license for a public-paid, robotaxi service in San Francisco with no human drivers, on top of its continued service in Arizona. In June 2022, an American carmaker’s subsidiary initiated a paid driverless robotaxi service in San Francisco. Another key multinational autonomous player has been incrementally offering rides in Las Vegas since 2018, and in August 2022 the company began offering some new, EVs specifically designed for passenger comfort, and importantly, continues to rack up the driverless robotaxi miles in geofenced areas of Las Vegas.

Shifting to China, leading companies continue to push forward with autonomous driving programs in the country, and the government is very focused on the domestic companies being both local and global players.

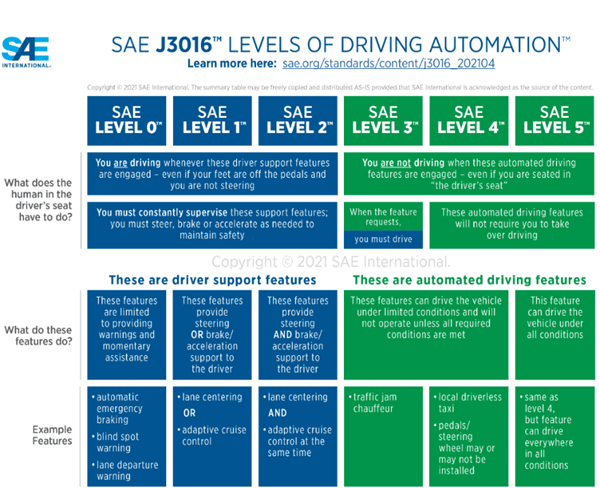

With regard to ADAS, it is important to recall that SAE International has established a foundational taxonomy for classifying ADAS and autonomous vehicle sophistication, as shown in the chart below.

With this in mind, a prominent auto company launched a Level 3 self-driving highway option in Germany, with plans for global availability. A leading US EV company continues to beta test its full self-driving system. There was also increasing penetration globally of both Level 1 and Level 2 ADAS, with the latter allowing the vehicle to self-drive in certain highway situations under the conditions outlined in the above chart. Virtually all manufacturers have some form of advanced ADAS plans and two Chinese companies have been very active, with a connectivity firm as a key ADAS technology contributor.

We expect ADAS to continue to grow and be a revenue driver for key suppliers. Robotaxis are a particular interest as we believe the dominant companies in the space are close to commercial viability. We also expect to get more information from areas such as autonomous trucking pilots being tested and autonomous grocery and other goods delivery vehicles. Still, we are realistic and expect some failures, such as in late 2022 when Argo AI closed the doors as its multinational co-owners did not want to commit more capital to the business. With the enormous amounts of capital required due to extended development period and challenges to achieve the end goal of autonomous vehicles, there will be more companies that exit the industry. Because of these risks, we continue to have high conviction in 2023 and beyond that ADAS Levels 1-3 remain the core revenue and growth driver within the industry.

The most realistic progression appears to be auto companies adding ADAS features to improve functionality, from driving assistance, to navigated autopilot on highways and eventually in cities, to finally fully autonomous driving. But the progression to autonomous driving will not be linear as there will be the usual setbacks along the way. Assuming the industry can get over the hurdles of technology and regulations, autonomous driving should become a major technological achievement in the passenger and commercial vehicle markets. And ideally these vehicles will be fully electric, so consumers get both safety and environmental benefits.

Electrification

In 2022, the penetration of electric vehicles was robust in key regions such as China, Europe, and the US, with China above 20% new electric vehicle penetration, Europe around 20% and the US 7%. We believe the penetration of EVs will continue to increase in all key regions during 2023. There will be more models being launched in key markets which will give consumers more choice than ever, and at many different price points.

Although China’s NEV subsidy ended in 2022, the government extended the sales tax exemption for NEVs through 2023, which should continue to incentivize consumers. And in China the domestic brands should continue to gain share due to their competitive models versus foreign brands which have been late to the market. So even though the market will be more competitive in 2023 versus 2022, NEV OEMs with strong brands, leading technologies and attractive pricing should be able to withstand the onslaught of new NEV models.

Considering other regions such as Europe and the US, we assume EVs will continue to gain share with more new models being launched by OEMs as well as the continuing purchase incentives in place. The incentives from the US Inflation Reduction Act should lead to EVs recording increasing penetration in 2023, on top of new model launches from OEMs such as two large American carmakers. Europe also has purchase incentives that make it attractive to buy an EV and many new models are being launched, so penetration should increase further in 2023. That said, the one area of concern in Europe, as well as in the US, is the macroeconomics. The former will be dealing with energy-supply risks and higher costs of energy, and how this will affect areas such as industrial activity, especially in Germany.

As the US moves ahead with its plans to onshore both the EV and battery supply chains, we will continue to monitor the progress of large battery suppliers, which are expanding capacity in the US. Recently, the US Department of Energy announced the first set of projects funded by the Biden Administration’s Bipartisan Infrastructure Law to expand domestic manufacturing of batteries for EVs and materials and components currently imported from other countries, as well as enhancing the electrical grid. The $2.8 billion in grants uses a portion of the $7 billion allocated to the domestic battery supply chain.

Lastly, another positive for electrification was that in November 2022, at the COP27 climate summit in Egypt, US Energy Secretary Jennifer Granholm agreed to target sale and production of only zero-emission, heavy-duty vehicles in the US by 2040. The non-binding memorandum of understanding (MoU) will aim for 30% zero-emission vehicle sales for heavy-duty vehicles, including school buses and tractors, by 2030, and 100% by 2040. The MoU was previously signed by 16 countries and endorsed by 60 state/local governments, with more expected to jump on board soon, according to Reuters.

Sharing

There was a strong recovery of rideshare volumes in 2022, particularly in the US, as consumer behavior trended towards pre-Covid usage, with the industry on track to meet or exceed 2019 trip volumes depending on the service provider. Despite pandemic headwinds easing, a slower recovery in driver supply has led to inflated pricing across the board for rideshare consumers and created a headwind to trip-volume growth. However, elevated driver incentives and earnings potential have led to signs of easing through the second half of the year. On the cost side, restricted capital flow to loss-making delivery competition, especially in Asia, and slower growth on tougher comparables, has led to a large degree of consolidation and cost rationalization as the sector aims to prove its potential for durable profitability. The washout and improved cost discipline from competitors have benefited larger, global players on delivery margin expansion.

As we look ahead to 2023, we expect easing headwinds to driver supply, such as tight a labor market, elevated vehicle pricing and fuel costs, as well as greater earnings potential for rideshare/delivery drivers compared to 2019, to improve driver volume. More drivers should improve bookings volumes via better per-ride pricing for consumers and provide further opportunity for margin expansion as driver incentives come down to normalized levels. Consumer behavior should also continue to trend positively as social recreational activity continues to recover, particularly on the West Coast of the US, which has lagged in its recovery thus far, but we remain wary of the macro-risk overhang on broader consumer spending.

Restaurant delivery growth should continue to slow but expansion of a well-established user base into grocery and alcohol delivery provides further levers to delivery growth, particularly as a tougher macro environment may push consumer food spending towards groceries compared to restaurants. Globally, the rate of growth in delivery and sharing should trend towards more normal levels as we believe volumes in the post-Covid world and the underlying demand for these services will continue to be positive. That said, we remain cautious on the overall segment and will be selective with our exposure.

Conclusion

2022 was a difficult year for technology stocks in general and for those industries that supply the mobility theme specifically. Supply-chain and logistical challenges that emerged during the Covid pandemic as a result of shifts in demand, labor shortages and structural factors have affected the key drivers of the mobility theme. This backdrop, however, provides opportunities as technology valuations settle near longer-term average support. We believe that the innovative energy among ADAS providers and their ability to advance the movement toward AVs underpin long-term growth potential. We expect new opportunities will unfold in 2023 once expectations reset in the first half.

Authors

George Saffaye

Global investment strategist

Robert C Zeuthen

Head of secular pod, portfolio manager

Frank J Goguen

Research analyst, portfolio manager

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. For additional Important Information, click on the link below.

Important information

This is a financial promotion. Issued by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Newton Investment Management Limited is authorized and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. 'Newton' and/or 'Newton Investment Management' brand refers to Newton Investment Management Limited. Newton is registered in England No. 01371973. VAT registration number GB: 577 7181 95. Newton is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940. Newton's investment business is described in Form ADV, Part 1 and 2, which can be obtained from the SEC.gov website or obtained upon request. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. You should consult your advisor to determine whether any particular investment strategy is appropriate. This material is for institutional investors only.

Personnel of certain of our BNY Mellon affiliates may act as: (i) registered representatives of BNY Mellon Securities Corporation (in its capacity as a registered broker-dealer) to offer securities, (ii) officers of the Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds, and (iii) Associated Persons of BNY Mellon Securities Corporation (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Mellon Investment Management firms, including Newton and (iv) representatives of Newton Americas, a Division of BNY Mellon Securities Corporation, U.S. Distributor of Newton Investment Management Limited.

Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any governmental entity) and are not guaranteed by or obligations of The Bank of New York or any of its affiliates. The Bank of New York assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection therewith. © 2020 The Bank of New York Company, Inc. All rights reserved.

In Canada, Newton Investment Management Limited is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Ontario and Quebec and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.