Key points

- We believe the new political landscape could prove positive for the UK gilt market, as the inflationary impact of Russia’s invasion of Ukraine fades and a degree of stability and certainty returns to markets.

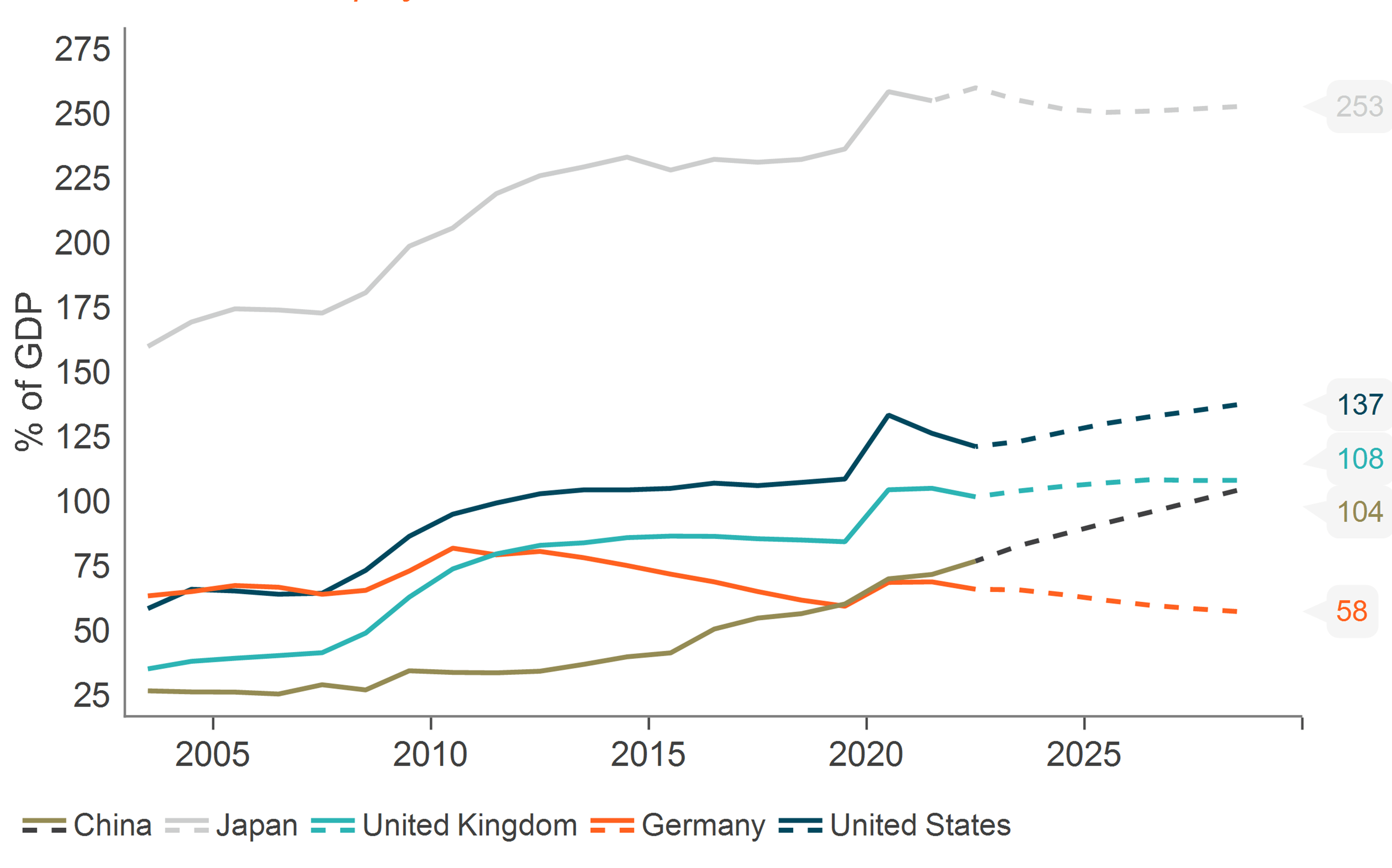

- The new government faces a tight fiscal situation, with a high debt-to-GDP ratio, elevated borrowing costs, and pledges to limit the scope for income-tax hikes.

- We believe the government will need to be prudent in its expenditure and may ultimately need to resort to other tax increases in the future.

- Ambitious plans to boost economic growth come via a significant housebuilding programme and a proposed national green energy fund.

- With near-term energy price rises a potential side effect of the green energy initiative, the government may need to convince the electorate that its plans will prove beneficial over the longer term.

The significant margin of victory achieved by the Labour Party at the recent UK general election was not a surprise, but how does it fit with our expectations for the UK’s gilt market and broader economy?

Overall, we anticipate that the new political landscape could prove positive for the gilt market over the near to medium term. Our view is that as the inflationary impact of Russia’s invasion of Ukraine continues to slowly roll out of the inflation data, the real yield now on offer from gilts looks more attractive than it has for some time.

UK growth has been anaemic despite a significant government budgetary overspend over the last few years. Labour ruled out income-tax hikes in its manifesto, and, now in power, the party is at great pains to explain that specific policies are ‘fully funded’, or ‘fully costed’. This indicates to us that the new government is wary of being labelled profligate as it may not receive the same leeway from much of the UK press as was afforded to its Conservative Party counterparts while in power. We anticipate that Labour may need to pick its expenditure battles wisely.

Spending constraint

In the latest quarterly report from the UK Treasury Debt Management Office (DMO) we note that the UK’s projected annual financing requirements are likely to call for further spending constraint. The UK debt-to-GDP ratio is expected to peak in 2025-26, while gross debt issuance should peak in 2025 at around £300bn, with a projected net-debt issuance of around £125bn. This elevated borrowing programme, initiated by the previous government, is now being serviced at higher borrowing costs as interest rates have risen to try to counter the recent period of high inflation (see chart below).

In the latest quarterly report from the UK Treasury Debt Management Office (DMO) we note that the UK’s projected annual financing requirements are likely to call for further spending constraint. The UK debt-to-GDP ratio is expected to peak in 2025-26, while gross debt issuance should peak in 2025 at around £300bn, with a projected net-debt issuance of around £125bn. This elevated borrowing programme, initiated by the previous government, is now being serviced at higher borrowing costs as interest rates have risen to try to counter the recent period of high inflation (see chart below).

Authors

Custom disclaimer

New line of text.